The prediction was straightforward: A rapid rise in interest rates orchestrated by the Federal Reserve would confine consumer spending and corporate profits, sharply reducing hiring and cooling a red-hot economy.

But it hasn’t worked out quite the way forecasters expected. Inflation has eased, but the biggest companies in the country have avoided the damage of higher interest rates. With earnings picking up again, companies continue to hire, giving the economy and the stock market a boost that few predicted when the Fed began raising interest rates nearly two years ago.

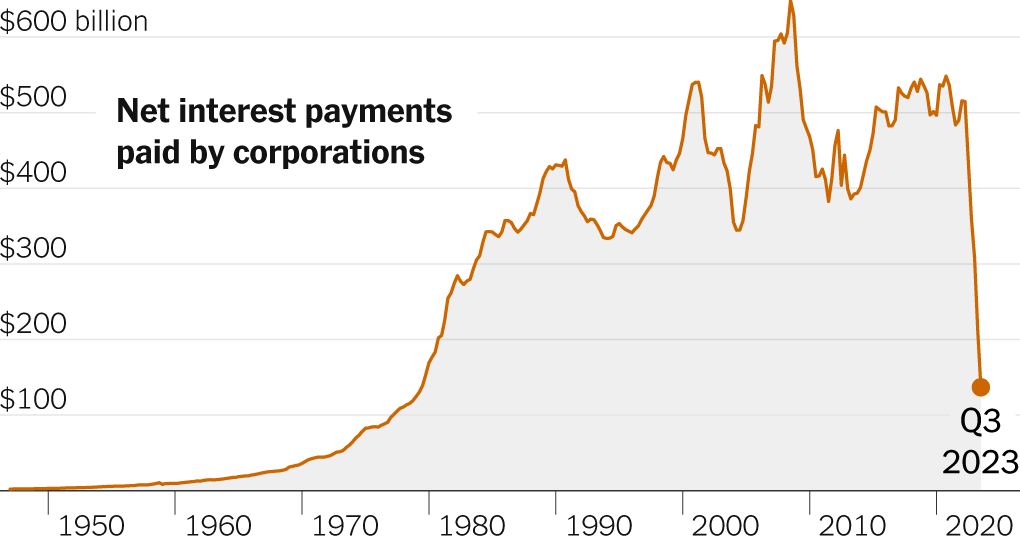

There are two key reasons that big business has avoided the hammer of higher rates. In the same way that the average rate on existing household mortgages is still only 3.6 percent — reflecting the millions of owners who bought or refinanced homes at the low-cost terms that prevailed until early last year — leaders in corporate America locked in cheap funding in the bond market before rates began to rise.

Also, as the Fed pushed rates above 5 percent, from near zero at the start of 2022, chief financial officers at those businesses began to shuffle surplus cash into investments that generated a higher level of interest income.

The combination meant that net interest payments — the money owed on debt, less the income from interest-bearing investments — for American companies plunged to $136.8 billion by the end of September. It was a low not seen since the 1980s, data from the Bureau of Economic Analysis showed.

That could soon change.

While many small businesses and some risky corporate borrowers have already seen interest costs rise, the biggest companies will face a sharp rise in borrowing costs in the years ahead if interest rates don’t start to decline. That’s because a wave of debt is coming due in the corporate bond and loan markets over the next two years, and firms are likely to have to refinance that borrowing at higher rates.

The junk bond market faces a ‘refinancing wall.’

Roughly a third of the $1.3 trillion of debt issued by companies in the so-called junk bond market, where the riskiest borrowers finance their operations, comes due in the next three years, according to research from Bank of America.

The average “coupon,” or interest rate, on bonds sold by these borrowers is around 6 percent. But it would cost companies closer to 9 percent to borrow today, according to an index run by ICE Data Services.

Credit analysts and investors acknowledge that they are uncertain whether the eventual damage will be containable or enough to exacerbate a downturn in the economy. The severity of the impact will largely depend on how long interest rates remain elevated.

“I think the question that people who are really worrying about it are asking is: Will this be the straw that breaks the camel’s back?” said Jim Caron, a portfolio manager at Morgan Stanley. “Does this create the collapse?”

The good news is that debts coming due by the end of 2024 in the junk bond market constitute only about 8 percent of the outstanding market, according to data compiled by Bloomberg. In essence, less than one-tenth of the collective debt pile needs to be refinanced imminently. But borrowers might feel higher borrowing costs sooner than that: Junk-rated companies typically try to refinance early so they aren’t reliant on investors for financing at the last minute. Either way, the longer rates remain elevated, the more companies will have to absorb higher interest costs.

Among the firms most exposed to higher rates are “zombies” — those already unable to generate enough earnings to cover their interest payments. These companies were able to limp along when rates were low, but higher rates could push them into insolvency.

Even if the challenge is managed, it can have tangible effects on growth and employment, said Atsi Sheth, managing director of credit strategy at Moody’s.

“If we say that the cost of their borrowing to do those things is now a little bit higher than it was two years ago,” Ms. Sheth said, more corporate leaders could decide: “Maybe I’ll hire less people. Maybe I won’t set up that factory. Maybe I’ll cut production by 10 percent. I might close down a factory. I might fire people.”

Small businesses have a different set of problems.

Some of this potential effect is already evident elsewhere, among the vast majority of companies that do not fund themselves through the machinations of selling bonds or loans to investors in corporate credit markets. These companies — the small, private enterprises that are responsible for roughly half the private-sector employment in the country — are already having to pay much more for debt.

They fund their operations using cash from sales, business credit cards and private loans — all of which are generally more expensive options for financing payrolls and operations. Small and medium-size companies with good credit ratings were paying 4 percent for a line of credit from their bankers a couple of years ago, according to the National Federation of Independent Business, a trade group. Now, they’re paying 10 percent interest on short-term loans.

Hiring within these firms has slowed, and their credit card balances are higher than they were before the pandemic, even as spending has slowed.

“This suggests to us that more small businesses are not paying the full balance and are using credit cards as a source of financing,” analysts at Bank of America said, adding that it points to “financial stress for certain firms,” though it is not yet a widespread problem.

Corporate buyouts are also being tested.

In addition to small businesses, some vulnerable privately held companies that do have access to corporate credit markets are already grappling with higher interest costs. Backed by private-equity investors, who typically buy out businesses and load them with debt to extract financial profits, these companies borrow in the leveraged loan market, where borrowing typically comes with a floating interest rate that rises and falls broadly in line with the Fed’s adjustments.

Moody’s maintains a list of companies rated B3 negative and below, a very low credit rating reserved for companies in financial distress. Almost 80 percent of the companies on this list are private-equity-backed leveraged buyouts.

Some of these borrowers have sought creative ways to extend the terms of their debt, or to avoid paying interest until the economic climate brightens.

The used-car seller Carvana — backed by the private-equity giant Apollo Global Management — renegotiated its debt this year to do just that, allowing its management to cut losses in the third quarter, not including the mounting interest costs that it is deferring.

Leaders of at-risk companies will be hoping that a serene mix of economic news is on the horizon — with inflation fading substantially as overall economic growth holds steady, allowing Fed officials to end the rate-increase cycle or even cut rates slightly.

Some recent research provides a bit of that hope.

In September, staff economists at the Federal Reserve Bank of Chicago published a model forecast indicating that “inflation will return to near the Fed’s target by mid-2024” without a major economic contraction. If that comes to pass, lower interest rates for companies in need of fresh funds could be coming to the rescue much sooner than previously expected.

Few, at this point, see that as a guarantee, including Ms. Sheth at Moody’s.

“Companies had a lot of things going for them that may be running out next year,” she said.

Emily Flitter contributed reporting.